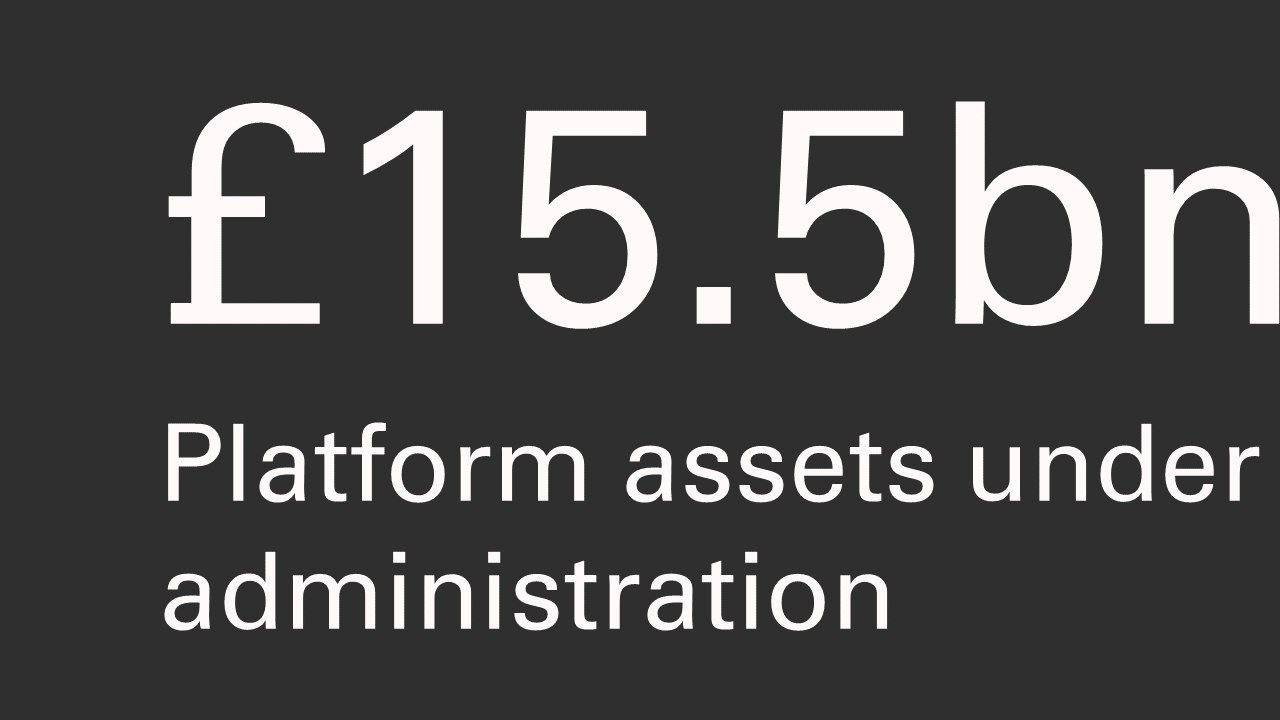

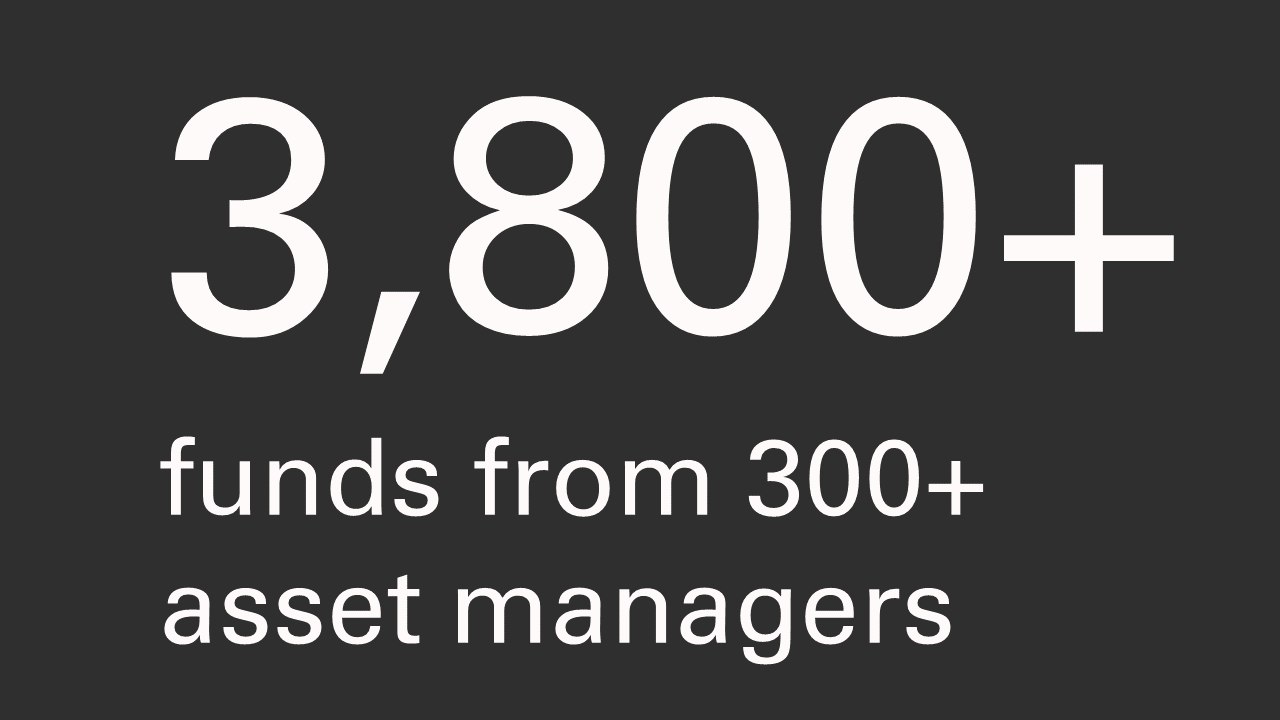

Platform in numbers

M&G Wealth Platform

The M&G Wealth Platform supports your investment proposition,

with the breadth and flexibility to meet your clients' needs as they

adapt and change.

Platform benefits

Family linking

A family group, including spouses, civil partners, cohabitees, parents, children, grandparents, grandchildren and step relations may benefit from a discount on our platform charge.

Model portfolios

Build and manage a range of model portfolios. From Model Portfolio Service funds, advisory and full discretionary from advisers or DFMs.

White labelling

Supporting your brand and proposition along with a range of services and features to provide a smooth, consistent and rewarding client experience.

Cash management

Manage cash in the way that works best for you and your clients. Set aside cash, protect cash from rebalances or use a cash account.

Third party integrations

We integrate with specialist partners to help keep your business efficient and connected while delivering tools and functionality to give clients a great investment planning experience.

Reporting

Access to full audit trail for each client account as well as a comprehensive Management Information (MI) reporting suite.

DFM access

We host over 100 DFMs on our platform, ranging from the big brands to specialist boutiques. If your preferred DFM isn't available, talk to us and we'll look to include it subject to agreement with them.

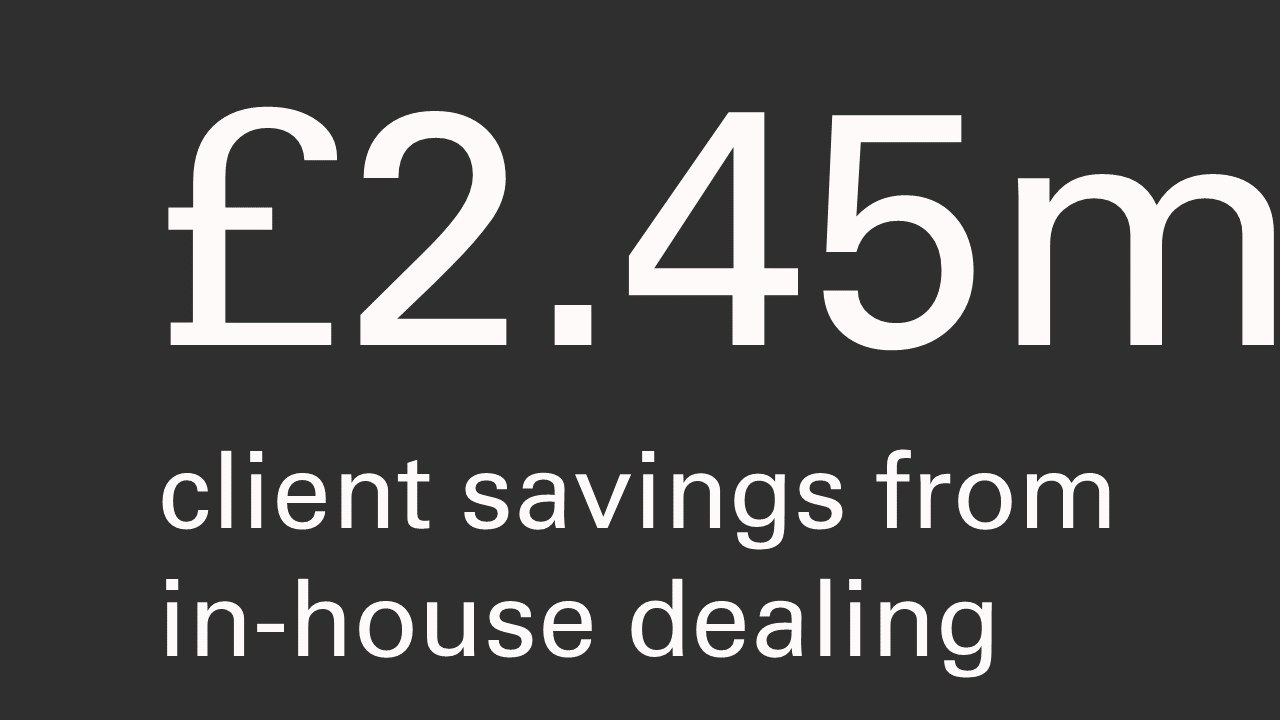

In-house dealing

We’re one of the few platforms with its own in-house exchange dealing desk. As a member of the London Stock Exchange, we can deal intraday so aren't limited to once a day bulk trades.

Pricing & charges

One platform price, no additional charges; no SIPP fees, no drawdown fees, no model portfolio fees and no exit fees. The single charge is based on the value of investments and cash in the portfolio and includes any taxes that may apply.

0.30%

Up to and including £1m*

0.10%

From £1m up to and including £3m

0.06%

From £3m up to and including £5m*

Contact us

Sales Team

If you'd like to know more about how M&G Wealth can support your business, our experienced staff are here to help.

Platform Customer Services

Please get in touch if you need help with the platform or have any questions.

Request a demo

Sign up for a platform demo and we will be in touch to show how we can support you and your business to provide good client outcomes.